But even though daily volatility of the two is at about the same level, it is a different type of volatility. While VIX moves quite a lot from day to day, over the long periods of time it stays in a relatively narrow range. Bitcoin on the other hand is volatility over the short term, and over the long term.

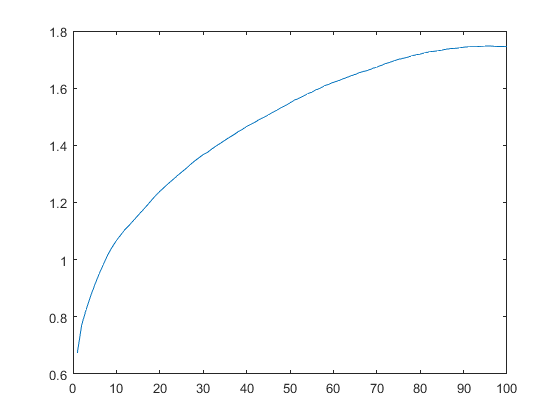

To illustrate the difference I will create a plot of term structure of volatility - how historical volatility evolves as a function of interval. So the first point in the plot will be annualized volatility calculated from one day returns, the second point will be from 2 day returns, etc.

The second chart is one for BTC USD rate I downloaded from Coindesk. What we see in the chart is just the opposite - volatility is increasing as function of time interval. Such behavior is common for trending time series, where positive moves are likely to be followed by more positive moves, and negative moves are likely to be followed by more negative moves.

So, if we were to extrapolate the historical behavior of these time series, and extend the charts beyond 100 trading days, we can make the following (and I'm sure quite imprecise) predictions: in a year from now 1 std move in VIX will be 30% ( 9.7-17.7 ), while 1 std move in BTC will be 190% ( 1,200-53,000 )

These forecasts are not serious forecasts, they just illustrate what some of the patterns we observe in the time series imply about future events.

No comments:

Post a Comment