All ideas above have been researched, and found some academic support - this paper by Avellaneda and Lipkin is an update of their seminal 2003 paper, another on pinning that contrasted optionable with non-optionable stocks, or this theoretical research into market feedbacks. However the empirical consensus is that on any particular stock this effect is rather small, and signal is too weak to be a stand-alone strategy.

I have been following options market on Deribit already for some time. Because options expire into an index, calculated from BTC/USD rate of 5 other exchanges, the hedging feedback mechanism would have a lot of friction, and probably does not exist. However, open interest could reflect market information in another way.

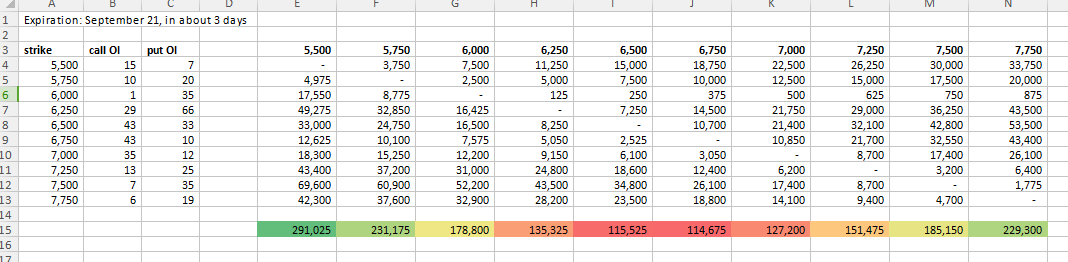

Here is a small spreadsheet where I calculated max pain strike for front (21st) and second (28th) expirations. Front is weekly, while second has been listed for 5 months now and has a much larger set of strikes. I trimmed the simulations in the second expiration but it does not effect the calculations.

Google sheet

The max pain strike for the front is 6750, followed closely by 6500, about 250 above where the market is now. For the second expiration, max pain strike is at 7000, followed by 6500. These ranges - 6500-6750 and 6500-7000 appear reasonable given recent market movement, but I would not read too much into them. We'll wait and see what the market actually does.

No comments:

Post a Comment