Few weeks ago BATS and T3 Index announced a launch of a

new equity volatility index based on SPY options. You may have seen ridiculous click-bait titles like "VIX Faces Challenge From Trading Robots Unleashed by Bats." About half-year ago I had the pleasure of meeting with Simon Ho, CEO of T3 Index, and have been corresponding with him about technical details of the index. So in this post I will cut out the hype and bring you the inside scoop about the differences between two indexes.

BATS launched an index created by T3 Index; and while the index is not tradable at this time, the plan is obviously to launch derivatives on it to complete with CBOE's monopoly. A little more than a year ago BATS moved into FX trading with purchasing Hotspot FX from KCG, and they are eager to expand to volatility as well. As far as I know there is no BATS futures exchange at this time, so watch out for the relevant filing.

Now, the differences:

1 - The index is based on SPY options as opposed to SPX. This makes index more robust, in terms of exchange presence (if one of the options exchanges stops disseminating quotes) and competing for liquidity. While SPY minimum tick are two times wider (0.01 on 1/10th of the index, vs 0.05 on SPX) effective quoted spreads are often narrower. I hope to follow up with another post comparing liquidity in SPX vs SPY vs CME SPX options.

2 - Price "dragging". This is (as far as I know) a completely new idea in index construction. What it means is that referenced options price will not be updated just because mid-quote changes, rather it will only update on a trade, or when quote goes completely outside of previous reference price. It is kind of like calculating a median of reference price with most current quote. If the bid-ask are fluctuating wildly this significantly reduces spurious jitters in index values, since values are updated only when there is a significant move. I should also note that this makes calculation of index to be path-dependant, meaning that you cannot take a snapshot of SPY options quotes intraday and calculate index value; rather you will need intraday history since the opening.

3 - SPYIX is calculated from regular monthly options, not weekly options. Last August VIX calculation failed during the first half-hour of trading, and the failure was attributed to lack of liquidity in 4th and 5th weekly series. While CBOE cannot revert index construction back to series options without losing face, T3 can benefit from this experience, and choose greater robustness. Related issue that is worth mentioning is "extrapolation" in the serial (pre-weeklies) VIX. Basically there were certain times when 30 days would fall outside of serial expirations, and VIX value was extrapolated. To avoid this issue, i.e. to always interpolate SPYIX is rolled closer to expiration (at 2 full days, as opposed to one week for serial VIX, if I remember correctly)

4 - Higher truncation price. SPX options have a minimum tick of 0.05, and that was also a value for strike truncation rule - if two consecutive prices of less than 0.05 (no-bid) are counted, no further strikes are used. SPYIX is uses the same cutoff despite SPY being 10x smaller than SPX. This makes any potential index manipulation much more expensive - as only "expensive" significant quotes are used in index construction.

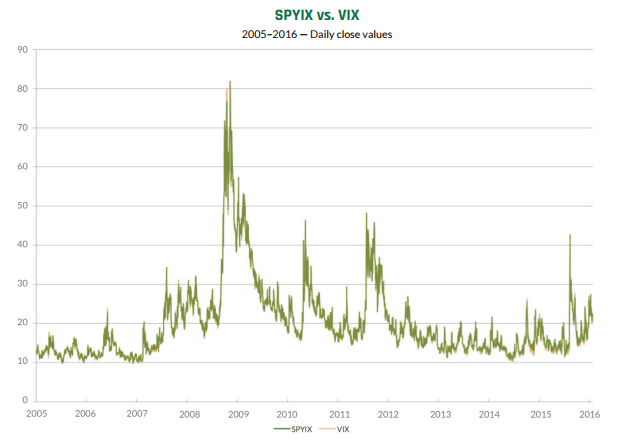

In fact robustness of the index is the main feature of SPYIX, and BATS explicity makes this point in the brochure "Reliability: The SPYIX is designed to withstand the most turbulent market conditions...when investors need it most." The rest of the time, both indexes values are in-line with each other - with SPYIX slightly above VIX ( mean 0.18, median 0.16, std 0.42)

Another technical difference, although that does not solve any robustness issues: SPYIX formula is the same as the VIX with only a small difference in how the forward adjustment is calculated. Basically both formulas have small adjustment terms, because we don't have a continuum of strikes, to account for when ATM forward is not exactly at a strike (which of course happens most of the time). VIX uses spot index value, and SPYIX uses interpolation with (another) robustness check. But meaning of the two formulas is essentially the same.

Another thing that I want to point out is a basis "difference". SPY pays quarterly dividend, and that has a small influence on index values. In theory before the ex-date SPYIX and VIX will diverge slightly, and will converge again right after the ex-date. In practice, this effect is not statistically significant (if you're interested in details, email me for exact numbers)

Additional resources:

SPYIX historical values,

fact sheet,

white paper,

sample calculation.

{kind=link}